Getting Started with Python Backtesting: How to Validate Your First Trading Strategy

Learn what backtesting is, why it matters, and how to do it in Python. A hands-on guide using a moving average strategy, calculating returns, Sharpe ratio, and maximum drawdown.

What Is Backtesting?

Backtesting is the process of applying an investment strategy to historical data to see whether it would have been profitable.

For example, suppose you create a rule: “Buy when the 20-day moving average crosses above the 60-day moving average.” You apply this rule to 5 years of historical data to simulate whether it would actually have made money.

Why is it necessary?

- What sounds good in your head is often very different from actual results

- Many strategies lose money once fees and slippage are accounted for

- A strategy not validated by data is no different from gambling

Setup

pip install pandas yfinance matplotlib numpyStep 1: Prepare Data

import pandas as pd

import numpy as np

import yfinance as yf

# Bitcoin daily data for 3 years

df = yf.download("BTC-USD", period="3y")

df = df[['Close']].copy()

df.columns = ['close']

print(f"Data: {len(df)} days, {df.index[0].date()} – {df.index[-1].date()}")Step 2: Define the Strategy

Start with a moving average crossover strategy.

# Calculate moving averages

df['ma20'] = df['close'].rolling(20).mean()

df['ma60'] = df['close'].rolling(60).mean()

# Generate trade signals

# 1 = buy (hold), -1 = sell (cash), 0 = wait

df['signal'] = 0

df.loc[df['ma20'] > df['ma60'], 'signal'] = 1 # MA20 > MA60 → Buy

df.loc[df['ma20'] <= df['ma60'], 'signal'] = -1 # MA20 ≤ MA60 → Sell

# Actual position (assume entry at next day's open)

df['position'] = df['signal'].shift(1)

print(f"Buy signal days: {(df['position'] == 1).sum()}")

print(f"Sell signal days: {(df['position'] == -1).sum()}")Step 3: Calculate Returns

# Daily returns

df['daily_return'] = df['close'].pct_change()

# Strategy returns (only when holding a position)

df['strategy_return'] = df['position'] * df['daily_return']

# Apply transaction costs (0.1% per trade)

df['trade'] = df['position'].diff().abs() # Number of position changes

df['strategy_return'] -= df['trade'] * 0.001 # Deduct fees

# Cumulative returns

df['cumulative_market'] = (1 + df['daily_return']).cumprod()

df['cumulative_strategy'] = (1 + df['strategy_return']).cumprod()

# Results

market_return = df['cumulative_market'].iloc[-1] - 1

strategy_return = df['cumulative_strategy'].iloc[-1] - 1

print(f"Market return (buy & hold): {market_return:.2%}")

print(f"Strategy return: {strategy_return:.2%}")Step 4: Calculate Performance Metrics

Looking at returns alone is not enough. You also need to evaluate how much risk was taken.

Sharpe Ratio

The return divided by risk (volatility). Above 1 is acceptable; above 2 is good.

# Annualized Sharpe ratio

returns = df['strategy_return'].dropna()

sharpe = returns.mean() / returns.std() * np.sqrt(252)

print(f"Sharpe ratio: {sharpe:.2f}")Maximum Drawdown (MDD)

How much the portfolio fell from its peak to its trough. This represents the pain an investor would actually have had to endure.

cumulative = df['cumulative_strategy']

peak = cumulative.cummax()

drawdown = (cumulative - peak) / peak

mdd = drawdown.min()

print(f"Maximum Drawdown (MDD): {mdd:.2%}")Win Rate and Average P&L

# Returns per trade

trades = df[df['trade'] > 0]['strategy_return']

win_rate = (trades > 0).mean()

avg_win = trades[trades > 0].mean()

avg_loss = trades[trades < 0].mean()

print(f"Win rate: {win_rate:.1%}")

print(f"Average win: {avg_win:.3%}")

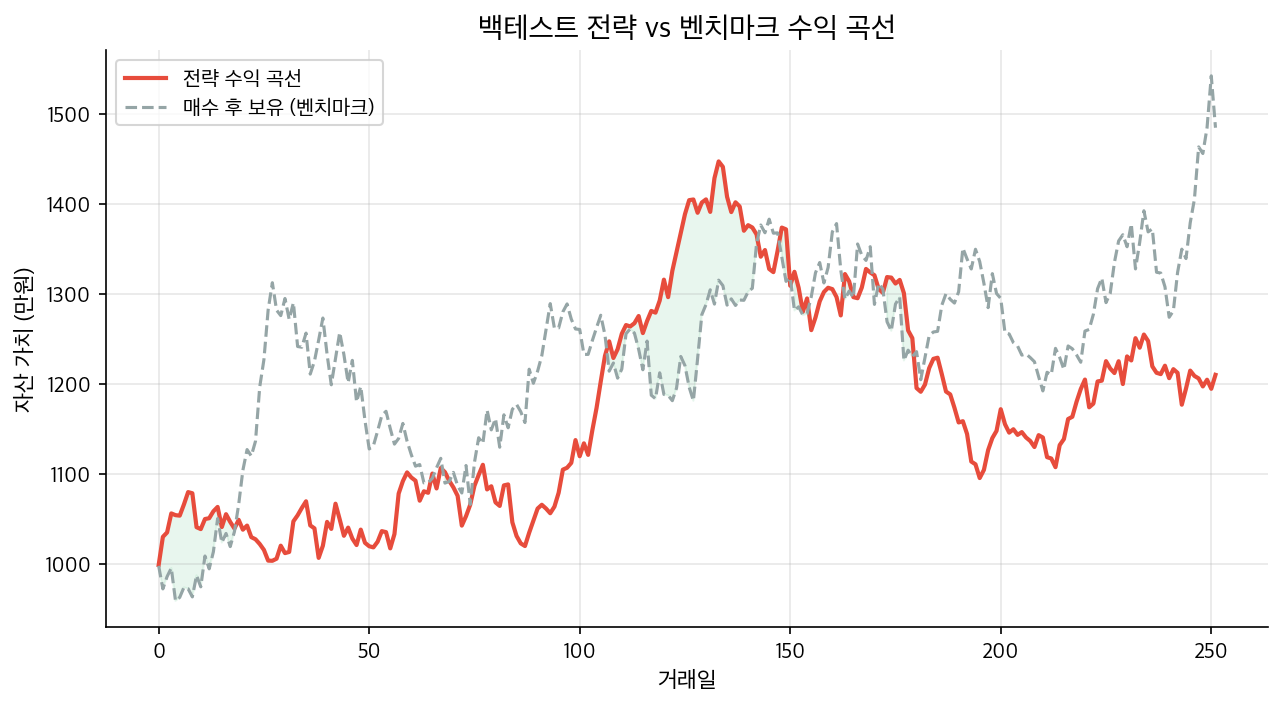

print(f"Average loss: {avg_loss:.3%}")Step 5: Visualize the Results

import matplotlib.pyplot as plt

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(14, 8), sharex=True)

# Cumulative return comparison

ax1.plot(df.index, df['cumulative_market'], label='Market (Buy & Hold)')

ax1.plot(df.index, df['cumulative_strategy'], label='Strategy')

ax1.set_title('Cumulative Return Comparison')

ax1.legend()

ax1.grid(True, alpha=0.3)

# Drawdown

ax2.fill_between(df.index, drawdown, 0, alpha=0.3, color='red')

ax2.set_title('Strategy Drawdown')

ax2.set_ylabel('Drawdown (%)')

ax2.grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('backtest_result.png', dpi=150)

plt.show()Key Pitfalls When Interpreting Backtest Results

Overfitting

If you iterate through parameter combinations (20-day, 60-day, etc.) to find the one with maximum profit, you likely have a strategy that only fits the past. If results change dramatically with a small tweak to the parameters, that is a warning sign.

No Look-Ahead Bias

Never assume you can trade at today’s closing price using today’s close. In reality you cannot know the closing price until after the close, so always assume entry at the next day’s open after a signal fires. Forgetting shift(1) introduces look-ahead bias.

Fees and Slippage

Excluding transaction costs inflates returns significantly. This effect is especially pronounced for high-frequency strategies.

Survivorship Bias

“Backtesting on Bitcoin gives great results” — that’s partly because Bitcoin survived. Running the same backtest on failed coins would give very different results.

Next Steps

This guide covers the most fundamental manual backtesting approach. To go further:

- Use a backtesting framework: Backtrader, Vectorbt, Zipline

- Walk-forward validation: Split data into training and test periods, then repeat iteratively

- Multi-asset portfolio: Strategies across multiple instruments rather than a single asset

- Risk management: Position sizing, stop-loss logic

Backtesting is not a tool for finding “a strategy that will make money” — it is a tool for confirming “this strategy does not work.” The real value is filtering out strategies that fail to pass.

Related Posts

Backtest Overfitting Prevention: Walk-forward vs Purged K-Fold Comparison

What to Look at Before IC When Combining Factors

What Is Quantitative Investing? A Beginner’s Guide for Individual Investors

Related Posts

Newsletter

Weekly Quant & Market Insights

Get market analysis, quant strategy ideas, and AI & data tool insights delivered to your inbox.

Subscribe →