The Magic of Compound Interest: How the Rule of 72 Tells You When Your Money Doubles

Understand the power of compound interest and learn how to use the Rule of 72 to quickly estimate when your investment will double. A beginner-friendly guide with real-life analogies and practical examples.

Compound interest has been called the “eighth wonder of the world.” After reading this guide, you’ll understand why it’s so powerful and learn a simple trick — the Rule of 72 — to estimate exactly how many years it takes for your money to double.

Understanding the Core Concepts

Compound Interest: The Snowball Effect of Money

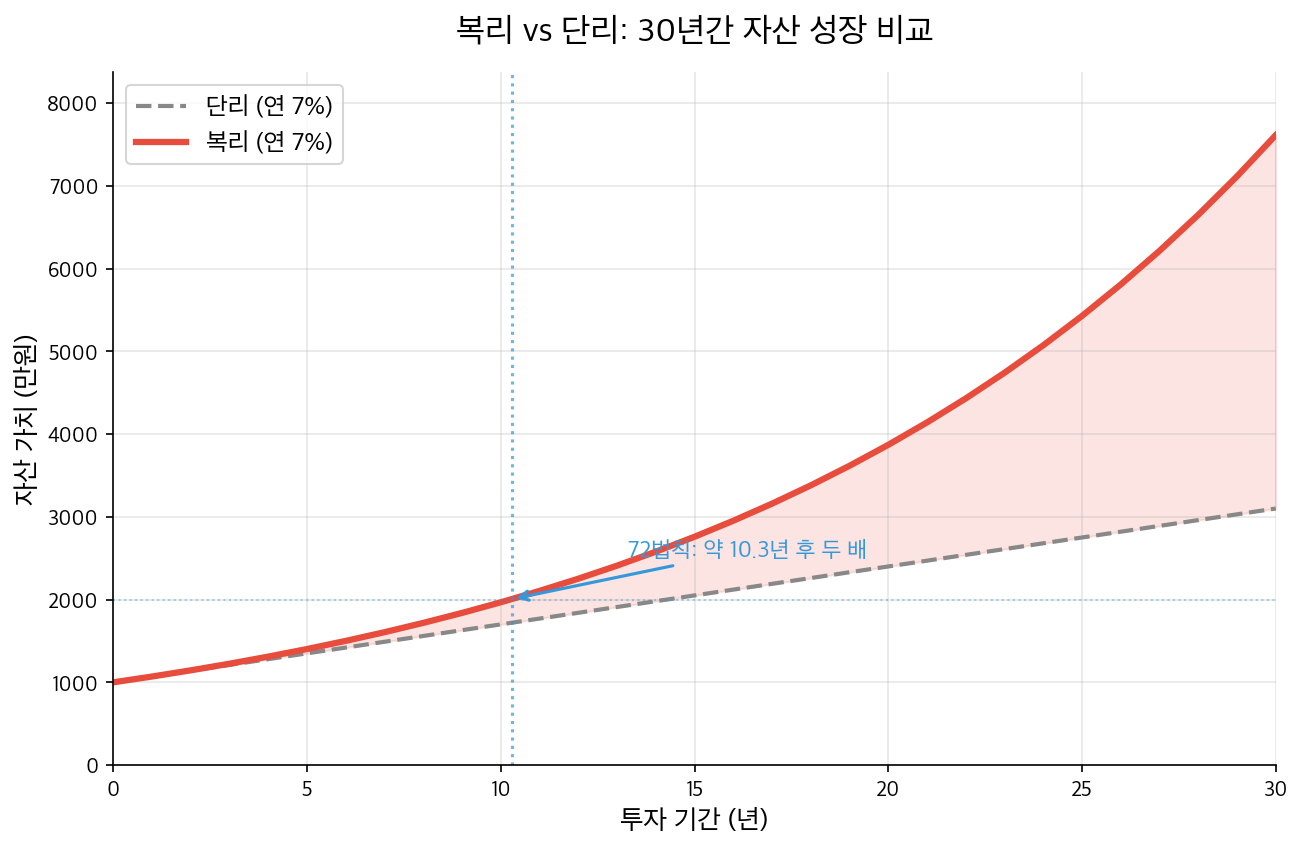

Compound interest means earning interest on your interest. Unlike simple interest (which only applies to your original principal), compound interest adds each period’s earnings back to the base, creating exponential growth over time.

Real-life analogy: Think of rolling a snowball down a hill. At first, it picks up just a little snow with each rotation. But as it grows larger, each turn adds a massive amount — and before you know it, the snowball is enormous. Compound interest works the same way: the longer you let it run, the faster your wealth accelerates.

The Rule of 72: A Quick Mental Math Shortcut

The Rule of 72 is a simple formula that estimates how long it takes for an investment to double at a given annual return:

72 ÷ Annual Expected Return (%) = Approximate Years to Double

For example, at a 6% annual return: 72 ÷ 6 = 12 years to double your money. No calculator needed.

Practical Applications

1. Setting Your Investment Timeline

You can reverse the formula to find the required return for a target timeline. Want to double your money in 15 years? 72 ÷ 15 = 4.8% — that’s the annual return you need. This helps you decide between conservative ETFs and higher-risk strategies.

2. Comparing Investment Products

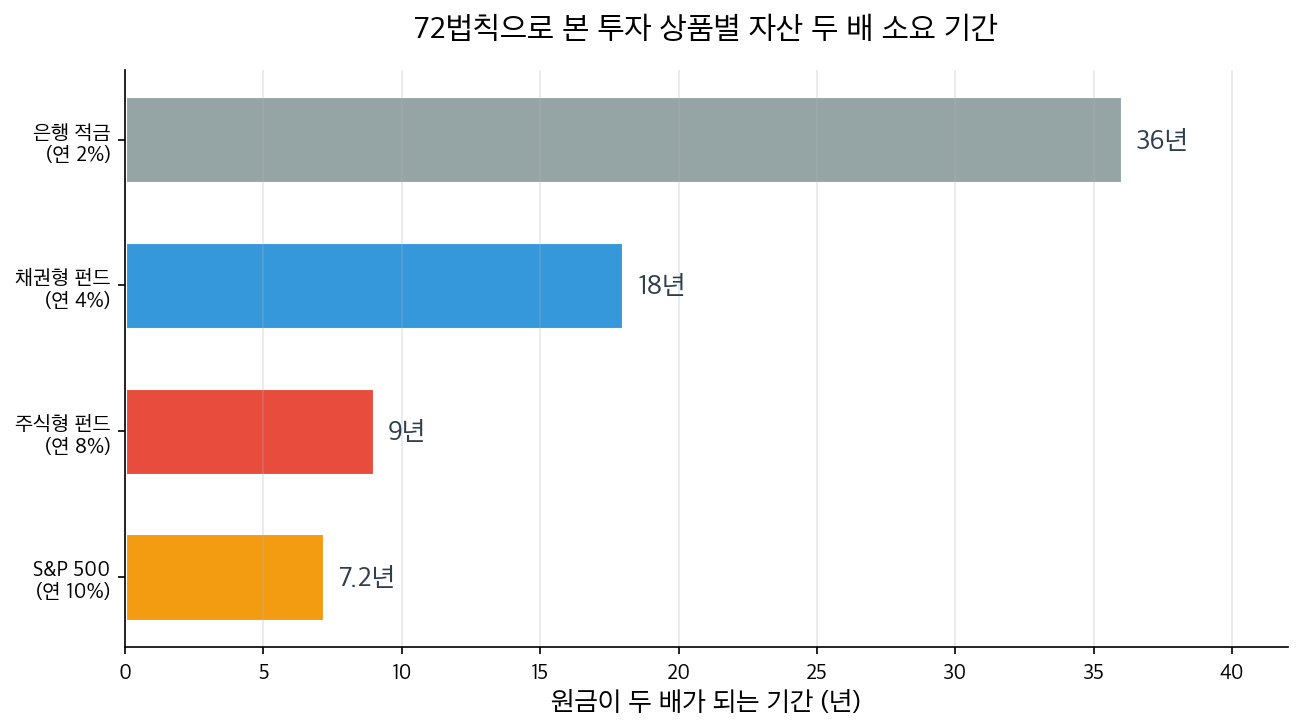

Quickly compare how long different products take to double your money:

- Savings account (2%): 72 ÷ 2 = 36 years

- Bond fund (4%): 72 ÷ 4 = 18 years

- Stock fund (8%): 72 ÷ 8 = 9 years

- S&P 500 (10%): 72 ÷ 10 = 7.2 years

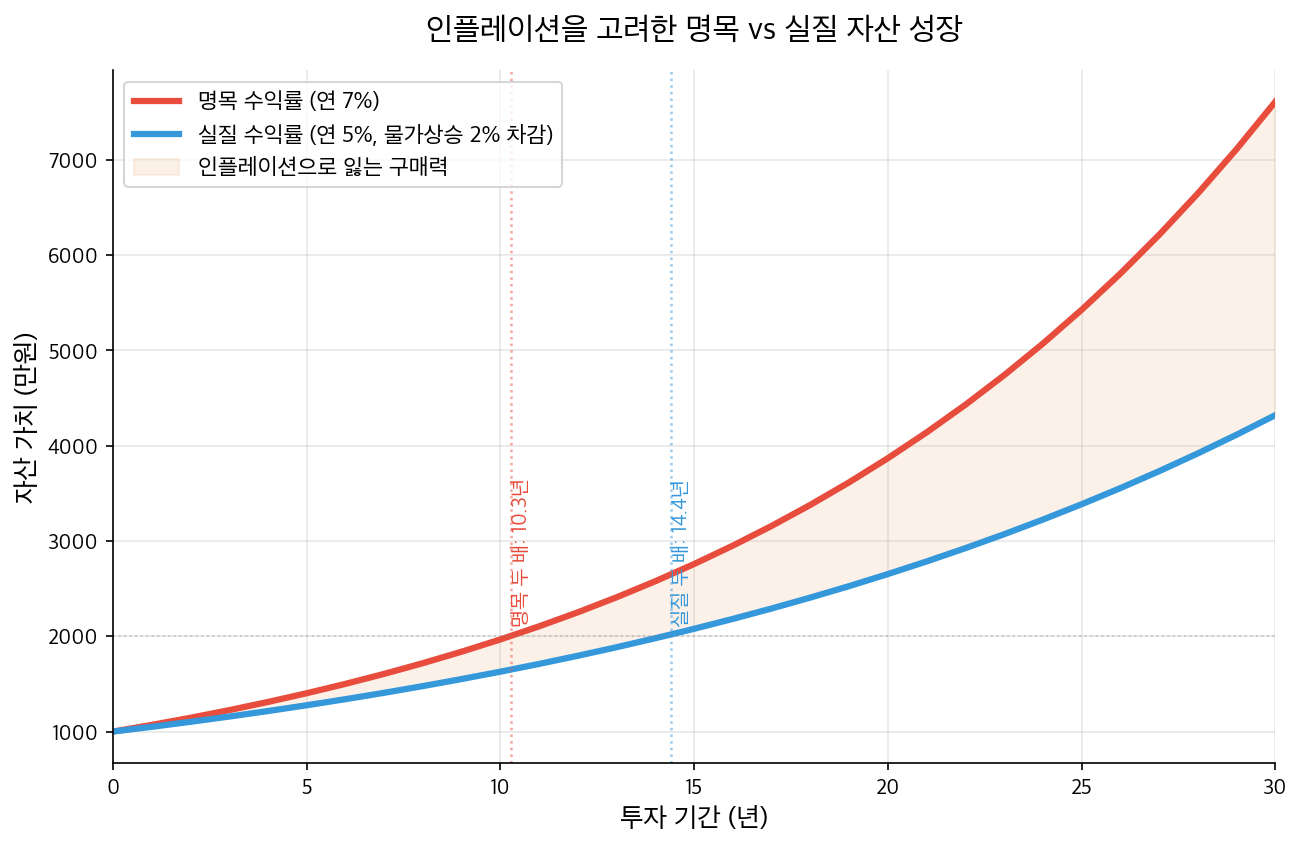

3. Accounting for Inflation

The Rule of 72 also works for real (inflation-adjusted) returns. If your expected return is 7% but inflation is 2%, your real purchasing power grows at ~5%. Time to double in real terms: 72 ÷ 5 = 14.4 years — over 4 years longer than the nominal estimate.

Risks and Disclaimers

The Rule of 72 is an approximation, not a guarantee. It assumes a constant annual return with annual compounding. In reality, returns fluctuate, and the rule works best for rates between 6% and 10%.

Most importantly, all investments carry the risk of loss. Past performance does not guarantee future results. Market volatility can extend your timeline significantly — or even result in losses. All investment decisions and their outcomes are ultimately your own responsibility.

FAQ

Q: How can I maximize the compound interest effect? A: Three factors matter: (1) Start as early as possible, (2) Invest consistently, (3) Maintain a reasonable return. Of these, time is the most powerful. Starting 10 years late means you’ll need dramatically more capital or higher returns to catch up.

Q: Does monthly vs. annual compounding affect the Rule of 72? A: Yes, slightly. Monthly compounding produces marginally more interest than annual compounding at the same nominal rate (higher effective rate). The Rule of 72 is based on annual compounding, so monthly-compounded investments will actually double slightly faster than the rule predicts.

Q: What matters most — initial capital, return rate, or time? A: All three matter, but time is the hardest to replace. You can’t go back and start earlier. High returns increase risk, and large initial amounts aren’t available to everyone. But starting small and starting early is a strategy anyone can choose.

Related Posts

Newsletter

Weekly Quant & Market Insights

Get market analysis, quant strategy ideas, and AI & data tool insights delivered to your inbox.

Subscribe →